The Fall of Private Blockchains: Why the Future of Blockchain Adoption Lies in Interoperable Networks

A short analysis on how enterprise blockchains are not a long term solution for traditional finance.

In the past few years, several large financial institutions have started tokenizing their securities. In this blurb we will be diving into some examples of their approach to asset tokenization, and critically analyzing how the trend of creating “enterprise blockchains” is actually counterintuitive to adoption of blockchain technology in the future.

Wall Street Giants Experiment with “Private Chains”

In late November, Goldman Sachs facilitated the issuance and settlement of a €100 million ($104m) digital bond for the European Investment Bank (EIB) on their private blockchain network. The 2-year syndicated bond issuance was settled instantly using central bank digital currency (CBDC) tokens issued by the Banque de France. The transaction is not novel. In fact, JPM has conducted $300B in intraday repo operations on their private chain (Onyx) since 2020, UBS reportedly has $35B in ADV on their Broadridge private chain, and the list goes on. Enterprise chains have been around as early as 2008.

But what if GS wanted to trade their tokenized bonds with JPM or UBS? What if they wanted to pledge their bonds as collateral to borrow from other liquidity providers / pools? What if they want to make investment products by combining other tokenized assets? What if they want to execute algorithmic trading strategies on multiple assets?

Why Private Chains Fall Short

Here’s where things get a little murky. Since GS, JPM, and UBS’ assets live on separate, private chains, the tokenized assets have different underlying data structures and therefore are not easily tradeable / transferrable among one another. Trading would again require manual settlement and reconciliation, or the development of entirely separate crossing network infrastructure to “bridge” these private chains. Yes, these institutions and many others building on private chains (see Symbiont, Axoni, etc.) may have the time and money to work with this clunky hybrid tech, but what’s the point of having a blockchain solution? A blockchain is a distributed database where all nodes store all data, so it is not optimized for latency and requires all nodes to update software individually. Deployment, latency, and administration is far easier for a simple distributed database compared to a blockchain ledger. If fast transaction settlement with immediate network partners is all institutions want, they are better off NOT using blockchain technology.

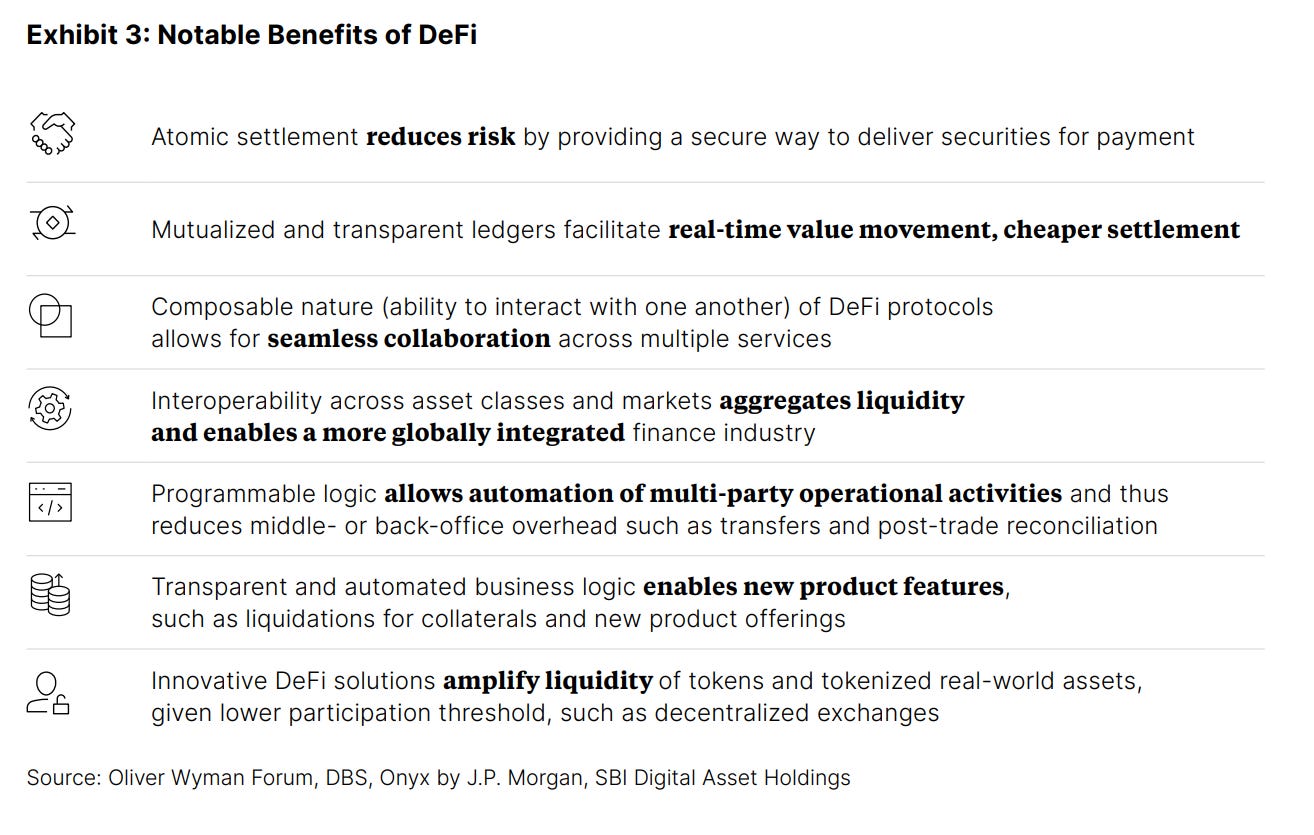

The words private and blockchain are almost oxymoronic, as most of the benefits of blockchain are derived from their public accessibility and use. Transparency, composability, multiparty transaction automation — these all come from public blockchain applications. Programmable money is possible to such an extent on public blockchains everyone agrees to the “same program” so to speak. Take decentralized finance (Defi) protocols, for example. Defi is made possible by the fact that tokenized assets all follow common data standards that can be executed on by smart contracts (think ERC-20). Private chains lose DeFi’s zero to one innovations including structured product creation, revolutionary automated market makers (AMMs), easy cross margining, and flash loans that are found on dApps. That’s why JPM, despite having their own enterprise chain (Onyx), tokenized and transacted Singaporean Government bonds on a modified version of AAVE Arc, a Defi protocol. In fact, JPM released a whole primer detailing how Defi technology will revolutionize finance.

Another element that Defi has in its favor is that the underlying infrastructure, public blockchains, allow for trustless verification and acceptance of transactions from a large network of distributed validators. On private chains, there are a very limited set of validators, and they are often limited to the institutions that create these networks. This creates issues from a legal perspective. Any actor that transacts on these private networks is implicitly trusting the central party that manages the chain to maintain an accurate record of trades, and to keep them manipulation free. This gives disproportionate power to the manager of such a network, and makes it unlikely that other financial institutions will trust other private chains with transactions at scale unless they reconcile their own records in tandem (no point of implementing blockchain again). However, there is concession point to be made that security on private chains is better due to the permissioned nature of access. Private chains do not have to deal with issues like MEV on their order books. While the decentralized validator system is ultimately the ideal situation, these security concerns mean that supernets and app-chains dominate the public blockchain space for enterprise applications for now, however they are a far better intermediary to bridge onto public blockchain layers than current private chains.

Private blockchains only exist in the short term due to regulatory oversight concerns and cybersecurity. Even if banks would like to pursue innovation on public layers, they are hamstrung by regulation and reputation. Their technology strategy is unfortunately more reactive than proactive due to their size and bureaucracy. For this reason, we see private chains as early sandbox experiments for institutions to get comfortable ledgering tokenized assets for when they eventually migrate to public chains.

Despite this, we see some progressive firms with less restrictive mandates venturing into the unknown by tokenizing their own assets on public chains (see KKR with Avalanche) as well as buying tokenized assets on public chains (see Apollo on Provenance), proving that the financial industry sees outsized returns despite the risk they are taking on this infrastructure.

The Future Lies in Regulated Defi Infrastructure

So what’s the solution? Institutions must look to innovative “RegDefi Protocols,” or protocols that are building financial infrastructure on public blockchains with a regulatory and security first approach. With the rise of “app-chains” as well it is becoming easy to have both public and private applications work in tandem and maintain most of the benefits of decentralized blockchain technology. The the creation of revolutionary financial technology will come through builders on Defi bridging the gap to traditional finance, not in Tradfi creating an entirely new exclusive system on their own networks.

One protocol building on the frontier of RegDefi for institutions is Blockhouse Capital. They are building an institutional DEX for bonds and credit derivates to bring liquidity and transparency to the nearly $226T international credit market. For more info on Blockhouse, visit our site.

Works Consulted:

The Inspiration — https://www.coindesk.com/business/2022/12/11/goldman-sachs-is-trying-to-make-blockchain-bonds-happen/

JPM Onyx Repo — https://www.coindesk.com/business/2022/11/23/singapore-bank-dbs-completes-fixed-income-trade-on-jpmorgans-blockchain-network-onyx/

UBS Broadridge Repo — https://www.thetradenews.com/ubs-joins-new-blockchain-based-repo-platform-from-broadridge/

Issues with Private Chains — https://www.coindesk.com/markets/2018/09/27/how-i-lost-my-faith-in-private-blockchains/

JPM Institutional Defi — https://www.jpmorgan.com/onyx/documents/Institutional-DeFi-The-Next-Generation-of-Finance.pdf

KKR Issuing Fund on AVAX —https://www.coindesk.com/business/2022/09/13/investment-giant-kkr-puts-portion-of-private-equity-fund-on-avalanche-blockchain/

Apollo Buying Tokenized HELOCs on Provenance — https://www.apollo.com/media/press-releases/2022/03-17-2022-120240961